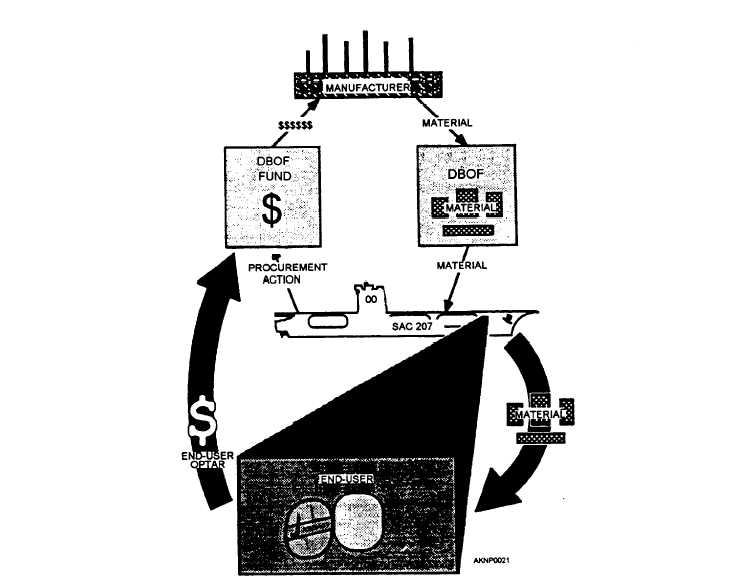

Figure 6-3.-The DBOF revolving fund.

them from material carried in other special account

classes. The SAC-207 activities include afloat units

such as tenders, repair ships, combat stores ships,

aircraft carriers, amphibious assault ships, and marine

air groups.

Transactions

The SUADPS-RT activities use DBOF to

requisition material for stock or direct turn-over (DTO)

by citing a SAC-207 fund code on the external

requisitions. When the material is received, it is

recorded as a receipt in the DBOF. When the material

is issued, the OPTAR fund of the end-user is charged to

reimburse the DBOF. This is done by citing the

activity’s UIC and the TYCOM’s fund code on the issue

document, resulting in a charge to the OPTAR funds and

a reimbursement to the DBOF. For DTO receipts, the

SUADPS-RT computer will process the receipt into the

SAC 207 fund and generate a charge to the end user’s

OPTAR fund.

When a SUADPS-RT activity issues material to an

end-use funded activity, charges are made to the

receiving activity’s OPTAR by citing the activity’s

OPTAR and the TYCOM’s fund code on the issue

document. This results in a charge to the customer’s

OPTAR and a reimbursement to the DBOF.

When there is an issue of DBOF material from one

SUADPS-RT activity to another SUADPS-RT activity,

the requisition is processed as an Other Supply Officer

(OSO) transfer.

6-11