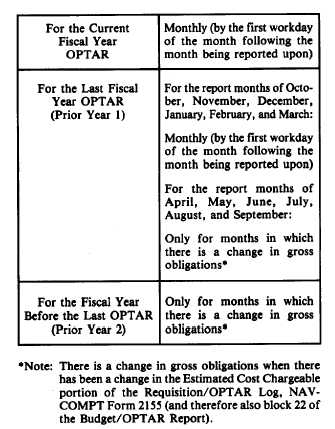

Document Transmittal Report, NAVCOMPT

Form 2156, on the last day of each month for

current fiscal year OPTARs. SUADPS OPTAR

holders only submit detail unfilled order (obliga-

tion) documents for some of their transactions

(for example, reimbursable OPTAR transactions,

flight operations, and services). Refer to figure

2-8 for the frequency of submission of the OP-

TAR document transmittal reports.

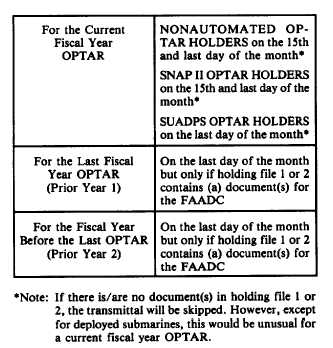

Budget/OPTAR Report

Under normal circumstances, the message

Budget/OPTAR Report, NAVCOMPT Form

2157, is used to report Budget/OPTAR Report

data, However, when the operating unit is in the

immediate vicinity of the FAADC or during

periods of message MINIMIZE, the report is

prepared and submitted instead of the message

report. When prepared, the Budget/OPTAR

Report is submitted by hand or mail to the

FAADC, with a copy to the TYCOM, no later

than the first workday of the month following the

month to be reported. When a message report is

submitted, the report is sent to the FAADC, with

a copy to the TYCOM no later than the second

day of the month following the end of the month

being reported. In addition, when the message

report is submitted, the Budget/OPTAR Report

copy is NOT submitted. Refer to figure 2-9 for

Figure 2-8.-Frequency of submission of the OPTAR

Document Transmittal Report, NAVCOMPT Form

2156.

Figure 2-9.-Frequency of transmittal of the Budget/

OPTAR Report, NAVCOMPT Form 2157.

the frequency of transmittal of the Budget/OP-

TAR Report.

FAADC TRANSACTION LISTINGS

The designated fleet accounting offices

(FAADCLANT and FAADCPAC), as the

authorization accounting activities, perform the

official accounting for OPTARs granted to ships,

aviation squadrons, and other commands, as

assigned. One part of the accounting process

performed for each OPTAR holder is the

matching of unfilled order documents transmitted

by OPTAR holders with the corresponding expen-

diture documents received from supply activities.

The reconciliation process results in the pro-

duction of listings that provide a report of

transactions affecting the OPTAR holder’s funds.

Some of these listings are submitted to the OP-

TAR holder for review and processing. Copies of

the listings, annotated with the action taken, are

returned by the OPTAR holder to the FAADC

so the official accounting records can be correctly

2-13