Four interrelated subsystems make up the

RMS to meet the objectives of the DOD. They

are as follows:

Programming and budgeting

Management of resources for operating units

Management of inventory and similar assets

Management of acquisition, use, and disposi-

tion of capital assets

The first, third, and fourth items are ap-

plicable primarily at the department, bureau, or

inventory manager level. The AK would be most

concerned with the second item. Current guide-

lines for the management of resources for

operating units are found in Financial Manage-

ment of Resources Operations and Maintenance

(Shore Activities), NAVSO P-3006, Financial

Management of Resources Fund Administration

(Operating Forces), NAVSO P-3013-1, and

Financial Management of Resources Operating

Procedures (Operating Forces), NAVSO P-3013-2.

OBJECTIVES

The basic objectives of the RMS, as applied

to operating units, are as follows:

l To determine the cost of operation of an

activity in terms of total resources consumed or

applied.

l To establish a system of controls that will

be of maximum value to commanders. Com-

manders use these controls to assure that resources

are used effectively and efficiently in the

accomplishment of the mission of the activity.

l To furnish operating budget grantors and

other levels of management, up to and including

the Navy Comptroller, that degree of financial

information necessary for effective coordination

and control of resources.

These objectives are achieved by implementa-

tion of the planning, programming, and budgeting

system and the use of such functional terms as

funds, appropriations, expense operating budgets,

responsibility centers, cost centers, expense

elements, and OPTARs. With an understanding

of the interlocking functions of all these factors,

the fiscal side of supply becomes a clear and

purposeful system. The material presented in this

TRAMAN provides the necessary background

information. Perhaps AKs may not be personally

involved in the consolidation of budget estimates;

however, it will be helpful if they know how the

process is carried out and how the action taken

at higher levels may both depend upon and affect

what they do locally,

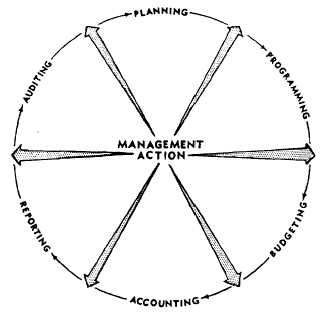

The RMS affects the entire management

process in the DOD. The following paragraphs

briefly define steps in the management process.

Figure 2-1 indicates the normal sequence of the

steps in the management cycle.

Planning in DOD is concerned with develop-

ing long- and midrange strategy and operational

concepts, objectives, and requirements based on

continuously projected appraisals of the world

situation and on technological and intelligence

forecasts.

Programming is concerned with setting

specific 5-year defense goals and the schedule for

achieving them, grouping functions and activities

sharing the same objectives into major programs,

and estimating resource requirements for each.

Budgeting is the function of formulating

1-year projections of resource requirements for

programs, balancing priorities in the competition

for limited resources, and obtaining associated

funds.

Accounting is the function of measuring the

results of performance (progress and status of

Figure 2-1.—Department of Defense management process.

2-3